Some of the most important advice I've ever given was advice a client didn't want to hear, and it cost him (and me) more than either of us expected. I'd love for you to watch the short video below before you keep reading. It's a story I don't tell to scare anyone. I tell it because I think it's one of the most honest illustrations I have of what it looks like when the numbers are right, and the emotions win anyway.

What Happened

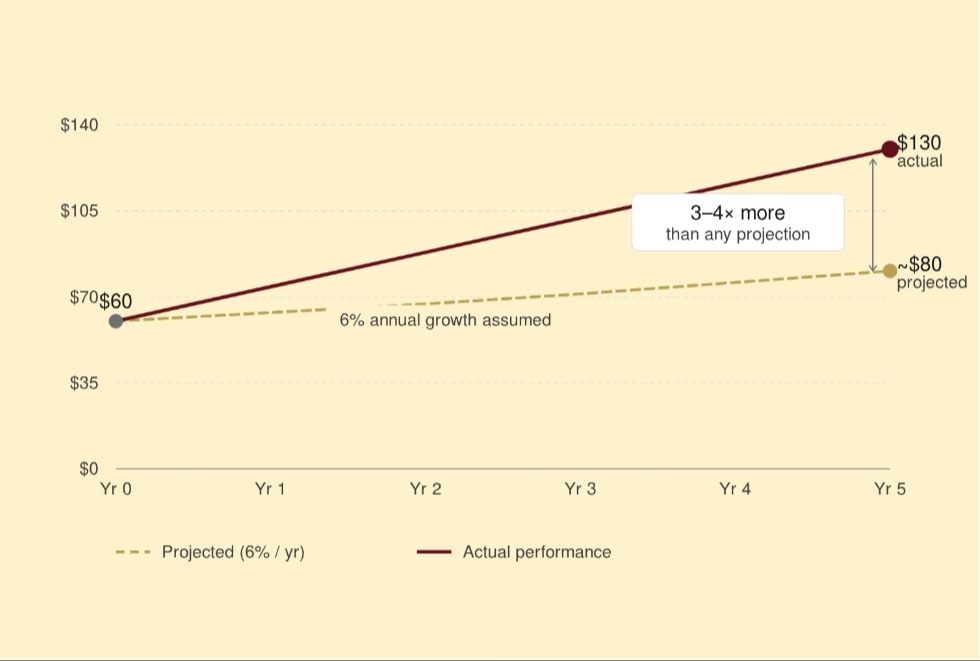

I had helped a client negotiate his way into a VP role at a company. The stock had already run from $16 to $60 in the six months before he joined, so I pushed hard in the negotiation for more options because the higher the stock climbs before you get in, the more risk you're absorbing, and the more you need to be compensated for that.

Over the next four to five years, the stock went to $130. That was three to four times more than we had ever projected. The man had more money sitting in his equity position than he had ever dreamed of seeing in his life.

***This chart is for illustrative purposes only. Numbers are approximate.

So, I went back to see him four months in a row. In the first conversation, I told him to sell everything. The second, I said to sell 75%. Third, let's at least do 50%. The fourth time, I asked him to take 25% (just one quarter of his position) off the table.

He fired me. He told me the stock was going to double again from there, and he didn't want to hear it anymore.

That stock has never seen $130 again. It fell all the way into the twenties and thirties before eventually clawing back to around $90, which is where it sits today at a five-year high.

He's going to be okay. He stayed at the company longer than we ever anticipated, and he'll still be financially independent, but he passed on the opportunity to take $20 million off the table. It wasn’t because the math was complicated, but because at that moment, the story in his head felt more real than the plan we had built together.

I've thought about that situation a lot over the years, and what I keep coming back to is this: my job isn't to tell clients what they want to hear. It's to be willing to have the hard conversation, even when it costs me the relationship, because that's what the moment demands.

Let me walk you through the framework I use when I'm sitting across from an executive who has significant equity on the line and a decision to make.

Step One: Get Clear on What You Need

Before we ever talk about upside, I want to know what this money actually needs to do for you and your family. What does genuine financial security look like? What does it cost to make your household untouchable regardless of what happens to your career, your company, or the market?

What are the things that are non-negotiable, like the kids' education, the mortgage, the retirement you've been building toward? What's your real timeline, not the one you're hoping for but the one that accounts for the unexpected?

When your equity position can fund that number, don’t ignore that signal. Does it mean sell everything? Of course, no. We do, however, encourage clients to consider the impact of taking some chips off the table to protect a meaningful piece of it. The moment you have enough to be truly secure, the calculus on holding changes completely. You're no longer investing as much as you're speculating. There's nothing wrong with speculation, as long as you know that's what you're risking.

Step Two: Get Honest About What You Want

Once we've established the floor, I want to talk about the ceiling.

What does the aspirational version of your financial life look like? We like to use the phrase “Envizion More”. We work with a lot of executives who have a vague sense that more is better but haven't actually defined what "enough" means to them. When you haven’t gotten clear on a truly compelling vision for life beyond your balance sheet, it's almost impossible to make a rational decision about when to sell.

I'll also ask something that sounds simple but usually lands hard: how much more upside do you actually need? If you've already made three times what you projected (or if the position has given you more than you ever thought it would), what are you really holding out for? Is that worth absorbing the full downside if the story changes?

I'm not trying to talk anyone out of believing in their company. I've just seen enough of these situations to know that the conviction that makes someone a great executive (the belief that the best is still ahead) can be the very thing that costs them everything they've already earned.

Step Three: Build a Plan That Protects You and Keeps You in the Game

This is where it gets practical. The goal isn't to sell everything and walk away. The goal is to take chips off the table in a way that's systematic so that you're still participating in the potential upside, but you're not betting everything on it.

Here's how we think about it with clients:

- Pencil in real numbers if your portfolio hits a certain amount. How much do you want to take off the table to fund or protect the core vision?

- Hypothetically, if your stock were to 3 to 4x expectations, pick a number attached to your vision for your life and family and set a sell plan. You may never need it, but set the plan before you are watching your stock climb.

- Always be re-evaluating: What would I lose if my bet on growth is wrong? You may find that certain answers are unacceptable, while others are worth the gain.

The Conversation Worth Having

I kept going back to that client four times because I believed he deserved to hear it. That's what I think this work is supposed to look like. You don’t hire an advisor for their optimism, but you should hire someone willing to risk the relationship because the stakes are too high to stay quiet.

If you've got significant equity compensation and you're trying to figure out when to sell, how much to hold, and how to balance the upside you're still excited about against the security you've already earned, we’d love to have that conversation with you.